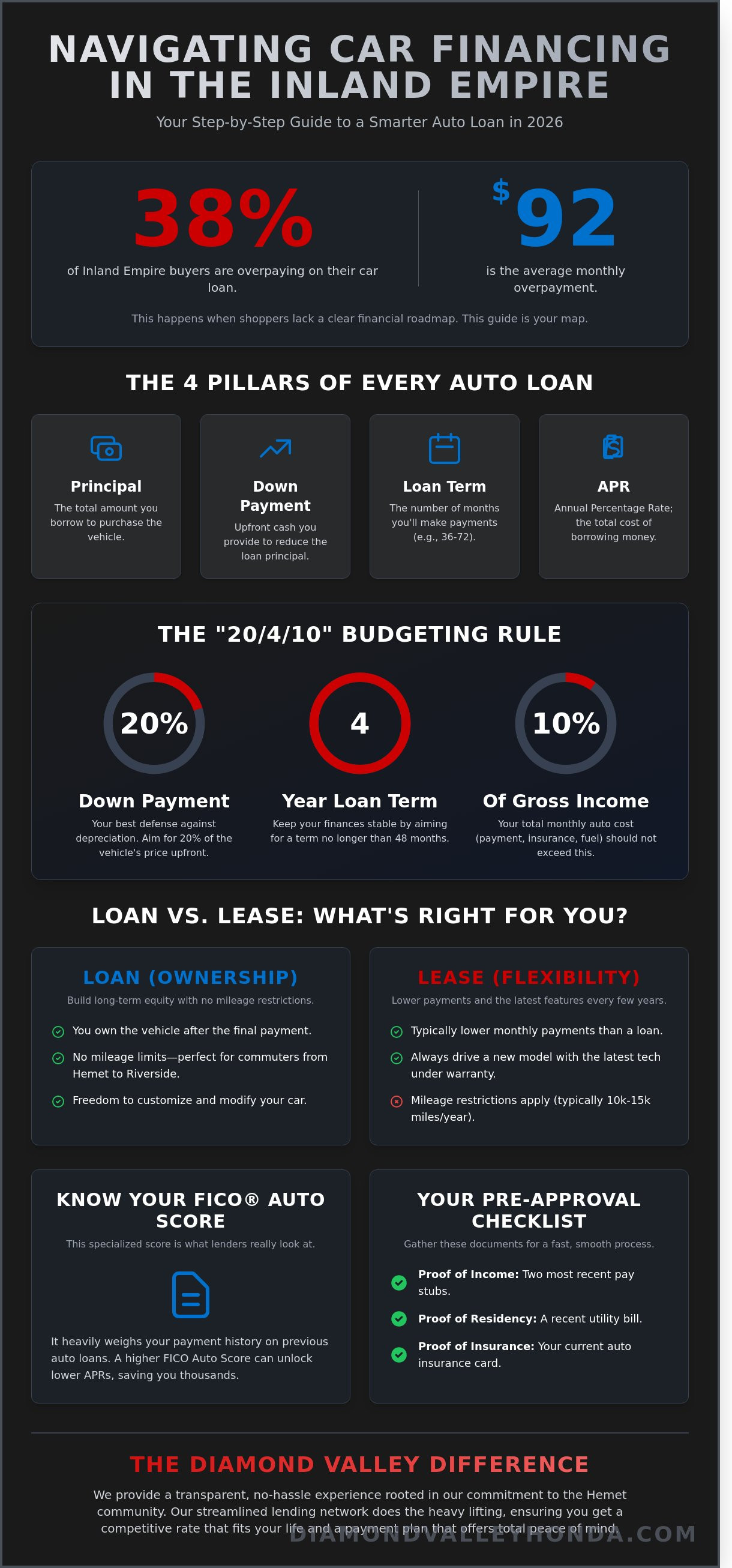

Recent 2026 market data shows that 38% of car buyers in the Inland Empire are currently overpaying on their monthly installments by an average of $92. This usually happens because shoppers dive into the process without a clear roadmap tailored for the current economic climate. We understand that staring down higher interest rates and choosing between a traditional bank or dealership financing feels stressful. It's natural to worry about your credit score or wonder if you're truly getting the most value for your hard-earned money.

The good news is that finding the best way to finance a car doesn't have to be a mystery. You deserve a transparent, neighborly experience that puts you in the driver’s seat of your finances. We've built this guide to help you navigate the local lending landscape with confidence and ease. You'll learn how to prep your credit for a top-tier approval and how to leverage specific Hemet incentives to keep your payments low. We provide a clear, step-by-step plan to secure a loan that fits your life. This ensures you walk away with a dependable vehicle and a payment plan that offers total peace of mind.

Key Takeaways

- Master your budget using the "20/4/10" rule and learn why your FICO Auto Score is the most critical number for Inland Empire drivers.

- Compare the advantages of local Hemet credit unions versus our streamlined dealership lending network to find your perfect financial fit.

- Discover the best way to finance a car by securing an online pre-approval and leveraging local market data for a higher trade-in valuation.

- Demystify complex terms like APR and loan principal with our step-by-step guide to making informed, confident financial decisions.

- Learn how the "Diamond Valley Difference" ensures a transparent, no-hassle experience rooted in our commitment to the Hemet community.

Understanding Car Financing in the Inland Empire

Securing a vehicle in Hemet means more than just picking a color; it's about making a strategic financial move that protects your savings. For most drivers in the San Jacinto Valley, auto financing serves as a vital tool to manage monthly cash flow while ensuring they have a reliable way to get to work or school. Finding the best way to finance a car starts with understanding how your money moves through the life of a contract. By spreading the cost of a vehicle over several years, you keep your liquid assets available for home repairs, emergencies, or local investments.

Every financing agreement relies on four primary pillars. The principal is the total amount you borrow to cover the vehicle's price. The Down Payment is the upfront cash you provide to reduce that principal immediately. The Loan Term defines how many months you'll make payments, typically ranging from 36 to 72 months. Finally, the Annual Percentage Rate (APR) dictates the cost of borrowing that money. Before signing, Understanding Car Financing Options helps you see how these variables interact to form your monthly obligation.

In 2026, many Hemet residents find that financing is smarter than paying full cash. With inflation stabilized at 2.1% and competitive lending rates available, keeping your cash in a high-yield savings account often yields better long-term results than sinking it all into a depreciating asset. We call this the Diamond Valley Difference. Our team focuses on transparent, localized lending that treats you like a neighbor rather than a credit score. We prioritize clear communication so you feel empowered throughout the process.

The Role of APR and Interest Rates in 2026

Interest rates fluctuate based on national economic trends and the collective credit health of our Inland Empire community. Annual Percentage Rate (APR) represents the total annual cost of borrowing, including interest and fees. Even a small shift in this number changes your total cost significantly. For example, a 1% difference in APR on a $35,000 loan can save a Hemet driver over $1,150 in interest charges over a 60-month term. We work with local credit unions and national lenders to find the best way to finance a car based on your specific history.

Loan vs. Lease: Which Fits Your Hemet Lifestyle?

Choosing between a loan and a lease depends on your daily habits. If you commute from Hemet to Riverside or Temecula every day, you likely rack up more than 15,000 miles annually. In this case, a traditional loan is usually better because it builds long-term equity without mileage restrictions. You own the vehicle once the final payment clears.

Conversely, if you prefer lower monthly payments and want the latest safety features every few years, a lease is a fantastic alternative. Many local drivers find that Honda lease deals provide the flexibility to upgrade to a new model every 36 months. This ensures you always have a dependable car under warranty for those hot summer drives across the 74 or 79 freeways.

Preparing Your Credit and Budget for a New Honda

The best way to finance a car begins long before you step onto our lot in Hemet. Your preparation determines the interest rate you secure and the long-term health of your bank account. Start by pulling your credit report, but don't just look at the standard number. Lenders often use a FICO Auto Score, which is a specialized version of your credit profile that emphasizes your history with previous vehicle payments. If you want a clear roadmap of this process, the Consumer Financial Protection Bureau provides a helpful step-by-step guide to auto loans that explains how lenders evaluate your risk.

Setting a realistic budget is the next vital step. We recommend the 20/4/10 rule of thumb to keep your finances stable. This means aiming for a 20% down payment, a loan term no longer than 48 months, and a total monthly automotive cost that doesn't exceed 10% of your gross income. In the 2026 Riverside County market, a solid down payment is your best defense against depreciation. It ensures you don't owe more than the car is worth, a situation often called being "underwater."

Before you visit us, gather your documentation to keep the process moving quickly. You will need:

- Proof of income: Your two most recent pay stubs or tax returns.

- Residency: A utility bill from the last 30 days showing your Hemet or San Jacinto address.

- Insurance: Current proof of insurance that can be updated to your new Honda.

Boosting Your Credit Score Before You Visit the Dealer

Small changes to your credit profile can lead to big savings. Review your report for errors like incorrect late payments or accounts that don't belong to you. Disputing these mistakes can result in a 20-point jump in your score within 30 to 60 days. This modest increase often moves you into a higher "tier" with Honda Financial Services, which can lower your interest rate by 1% or more. If you're planning a purchase, avoid opening new credit cards or taking out other loans for at least six months to keep your score stable.

Calculating Your Total Cost of Ownership in CA

A monthly payment is only part of the story. In Hemet, you must factor in the current 8.75% sales tax and California registration fees, which are based on the vehicle's value. Insurance rates in the Inland Empire can also vary, so get a quote for a 2026 Honda Accord or CR-V early in the process. You can use our car payment calculator to see how a larger down payment reduces your monthly obligation. Remember that maintaining your vehicle at our Hemet service center keeps your long-term costs lower by preventing expensive repairs down the road. If you're ready to see what you qualify for, you can apply for pre-approval online to save time at the dealership.

Comparing Your Options: Direct vs. Dealership Financing

Choosing the best way to finance a car often comes down to where you want to do the paperwork. You have two primary paths in the San Jacinto Valley. Direct financing involves securing a loan yourself through a Hemet credit union or a national bank before you visit the lot. This gives you a firm budget in your pocket, but it requires you to do all the legwork yourself. Dealership financing, however, allows Diamond Valley Honda to handle the heavy lifting by submitting your application to a broad network of over 20 different lenders simultaneously.

Many Hemet drivers mistakenly believe dealership loans always cost more than bank loans. This is a common misconception that doesn't hold up under scrutiny. Because we process a high volume of monthly transactions, banks often provide us with preferential pricing. We pass these savings directly to you. Our finance team acts as your personal advocate, comparing financing offers from multiple sources to ensure you get the most competitive terms available without driving all over town.

The convenience of "one-stop shopping" cannot be overstated. You can test drive a vehicle, value your trade-in, and sign your loan documents all in a single afternoon. This streamlined approach eliminates the stress of coordinating between a bank officer and a car salesperson. It's a faster, more efficient way to get behind the wheel of your next vehicle.

The Power of Honda Financial Services

Honda Financial Services (HFS) provides a unique advantage that traditional banks simply cannot replicate. As a captive lender, HFS offers manufacturer-backed incentives specifically designed to move inventory. For the 2026 model year, qualified buyers can often access 0.9% APR for 60 months on the new Honda Civic or 1.9% APR on the 2026 CR-V Hybrid. These rates are frequently lower than the prime rates offered by standard commercial banks. Being a captive lender allows Honda to offer these exclusive programs to loyal customers, providing a level of flexibility that helps you stay within your monthly budget while driving a brand-new car.

Local Credit Unions vs. National Banks

While some prefer the familiarity of their local Hemet credit union, Diamond Valley Honda maintains strong relationships with those same local institutions. We often access "wholesale" interest rates from these lenders. These rates are typically lower than the retail rates offered to the general public because the dealership handles the administrative processing for the bank. By using our network, you can still benefit from your favorite credit union's terms while enjoying the speed of our digital filing system. This hybrid approach represents the best way to finance a car for those who want local trust combined with modern efficiency. We work with both local neighborhood lenders and major national banks like Chase or Wells Fargo to find the perfect fit for your specific credit profile.

How to Secure the Best Auto Loan Rate in Southern California

Finding the best way to finance a car in the Inland Empire involves more than just picking a monthly payment that fits your budget. In 2026, savvy buyers in Hemet are looking at the total cost of credit to ensure long term savings. Securing a competitive rate requires a proactive approach before you even step onto the lot. By establishing a baseline interest rate through pre-approval, you gain the upper hand in negotiations and protect your wallet from unnecessary markups. We prioritize transparency, ensuring you understand every percentage point before you sign.

Leveraging Your Trade-In Value

Your current vehicle is a powerful financial tool. In California, your trade-in acts as a tax-free down payment because you only pay sales tax on the price difference between the new car and your trade. With used car demand in the Inland Empire climbing 14% since the start of 2025, your older model is likely worth more than you think. To secure the highest appraisal at our Hemet location, bring your complete service history and ensure all maintenance is up to date. This transparency helps us offer you top market value based on real-time 2026 regional data.

The Pre-Approval Advantage

Don't confuse pre-qualification with a hard pre-approval. While a pre-qualification gives you a ballpark estimate, a hard pre-approval involves a comprehensive credit review and provides a guaranteed rate. This status grants you cash-buyer confidence, allowing you to focus on the vehicle price rather than the financing terms. It's the most efficient way to shop. You can start this process from your living room by completing our online finance application to see exactly where you stand.

Before you finalize your deal, analyze the best way to finance a car by looking at these specific factors:

- Total Loan Cost: A lower monthly payment over 84 months often costs $3,000 more in interest than a slightly higher payment over 60 months.

- The Diamond Valley Difference: We maintain a strict policy of zero hidden fees and no high-pressure add-ons. Every line item is explained clearly.

- Local Market Comparison: Our team monitors rates across Riverside County daily to ensure our offers remain the most competitive in the region.

Once the paperwork is finalized, you'll drive home to Murrieta or Temecula with the peace of mind that comes from a transparent, neighborly deal. We believe in building relationships that last longer than a single loan term. Our goal is to make the process as smooth as the drive down Florida Avenue.

Ready to see your personalized rates? Apply for financing today and experience a stress-free path to your next Honda.

The Diamond Valley Difference: Transparent Financing in Hemet

At Diamond Valley Honda, we don't just sell cars; we support our neighbors. Our team lives and works right here in Hemet, just like you do. We understand the local economy and the specific needs of Inland Empire drivers. Finding the best way to finance a car shouldn't feel like a battle. That’s why we’ve committed to a "No-Hassle" pricing model. Our Finance and Insurance (F&I) offices operate with total transparency. You will see every number and fee clearly explained before you ever pick up a pen to sign.

Our relationship with you doesn't end when the contract is finalized. We aim to be your long-term automotive partner. To support our community in 2026, we offer several specialized programs tailored for local residents:

- Military Appreciation: We offer specific credits for active-duty members and veterans stationed at nearby bases.

- College Graduate Program: Recent grads can take advantage of lower rates to help jumpstart their professional lives in the Inland Empire.

- First-Time Buyer Initiative: We provide structured paths for those with no prior auto loan history to build their credit safely.

Expert Guidance for Every Credit Situation

We believe everyone deserves a reliable vehicle to get to work and school. If you have "less-than-perfect" credit, our team doesn't turn you away. We partner with a network of 18 different lenders specifically chosen to serve the Perris, Banning, and Menifee areas. These partnerships allow us to secure competitive terms even when traditional banks say no. Our finance managers are educators first, salespeople second. They will walk you through your credit report and explain how your monthly payment affects your overall financial health.

Protecting Your Investment

Driving in the Inland Empire often involves long commutes on Highway 74 or the 215 freeway. These miles add up quickly. To ensure your vehicle remains a dependable asset, we provide comprehensive Vehicle Service Contracts. These plans cover mechanical repairs long after the factory warranty expires. We also highly recommend GAP insurance for our local commuters. If an accident occurs and your vehicle is totaled, GAP insurance covers the "gap" between the insurance settlement and your remaining loan balance. This protection is critical for high-mileage drivers who may see faster depreciation. We want to ensure you have the best way to finance a car while maintaining total peace of mind.

Ready to start your journey with a team that puts your needs first? Visit Diamond Valley Honda today for a personalized finance consultation!

Take the Driver's Seat with Hemet's Trusted Finance Experts

Securing a reliable vehicle in the Inland Empire starts with a clear plan for your budget and credit. You've learned that comparing direct lenders against dealership options is the best way to finance a car while keeping your monthly payments manageable. By focusing on transparency and local market rates, you can avoid the stress often found at larger corporate chains. Diamond Valley Honda has served the Hemet community for over 20 years; we've helped more than 15,000 local drivers navigate the loan process with total clarity. Our expert finance team maintains a 4.8-star Google reputation by providing a 100% hidden-fee-free experience. We prioritize your peace of mind by breaking down every line item so you feel empowered before you sign. Whether you're looking for a 2026 Civic or a family-ready CR-V, our local experts are ready to build a plan that fits your life. Your next journey on the 74 or 79 starts with a smart financial foundation built right here in town.

Get Pre-Approved for Your Next Honda in Hemet Now

We're excited to help you get behind the wheel of a car you'll love for years to come.

Frequently Asked Questions

What is the minimum credit score needed to finance a car in Hemet, CA?

You can typically secure car financing with a credit score as low as 580, though higher scores unlock more favorable terms. While a score of 720 or above qualifies you for the lowest available interest rates, our finance team works with 15 different lenders to help those with scores in the 600 range. We look at your entire financial profile, including your two year steady employment history, to find a payment plan that fits your life.

How much should I put down on a new Honda in 2026?

You should aim for a down payment of 20% to achieve the most affordable monthly payments and offset initial depreciation. For a $30,000 vehicle, this means putting $6,000 down at the time of purchase. If that isn't feasible, a minimum of 10% is recommended by Honda Financial Services to improve your loan approval odds. Providing a solid down payment reduces your total loan balance and helps you build equity in your vehicle much faster.

Can I finance a car in California with no credit history?

You can finance a car without a credit history by utilizing specialized first-time buyer programs available at our dealership. These programs usually require a 10% down payment and proof of a steady income of at least $2,500 per month. We've helped over 200 local graduates and young professionals in Hemet establish their credit through these tailored options. It's a straightforward process that helps you build a strong financial foundation while driving a reliable vehicle.

Is it better to get a car loan from a bank or a dealership in the Inland Empire?

Securing a loan through Diamond Valley Honda is often the best way to finance a car because we compare rates from 20 different local and national lenders simultaneously. While a single bank offers only one set of terms, our finance center creates a competitive environment to find you the lowest APR. This one-stop approach saves you roughly four to six hours of visiting individual banks and gives you access to exclusive manufacturer incentives you won't find elsewhere.

What documents do I need to bring to Diamond Valley Honda for financing?

You need to bring your valid driver's license, your two most recent pay stubs, and a utility bill from the last 30 days to verify your residence. If you're trading in a vehicle, remember to bring the title or your current registration and a 10-day payoff statement from your current lender. Having these five specific documents ready allows our team to finalize your paperwork in about 45 minutes, ensuring a smooth and efficient experience from start to finish.

How do interest rates in Hemet compare to the rest of Southern California?

Interest rates in Hemet are highly competitive and generally stay within 0.25% of the average rates found in larger hubs like Los Angeles or San Diego. Our local lending partnerships allow us to offer aggressive rates that reflect the economic conditions of the Inland Empire. In 2026, buyers in Hemet often benefit from lower overhead costs at local dealerships, which frequently translates into more flexible financing terms and personalized service compared to high-volume metropolitan dealers.

Can I trade in a car that I still owe money on?

You can trade in a vehicle with an existing loan balance by letting our team handle the payoff process directly with your lender. We'll calculate the difference between your car's $18,000 trade-in value and your $15,000 loan balance to give you a $3,000 credit toward your new purchase. If you owe more than the car's current market value, we can often roll that negative equity into your new loan. This consolidated approach keeps your transition into a new Honda simple.

What happens if I want to pay off my car loan early?

You can pay off your auto loan ahead of schedule without any prepayment penalties or hidden fees at our dealership. Making extra payments toward your principal balance reduces the total interest you'll pay over the 60-month or 72-month term of your loan. This strategy can save you $500 or more in interest charges over the life of the contract. It's a smart financial move that gives you full ownership of your car sooner than originally planned.